Are you looking for a lightweight introduction to product management in fintech? Have you wondered why shipping fintech products takes more time than shipping other products? Or have you ever asked, “what sets fintech product management apart from other product management jobs?”

If the answer to any of the above questions is “yes,” this article will help you understand some of the foundations of fintech product management. Of course, this is a broad topic, so I will limit this post to topics that are critical but not as frequently discussed as I would like them to be.

Fintech Essentials and the Fintech Landscape

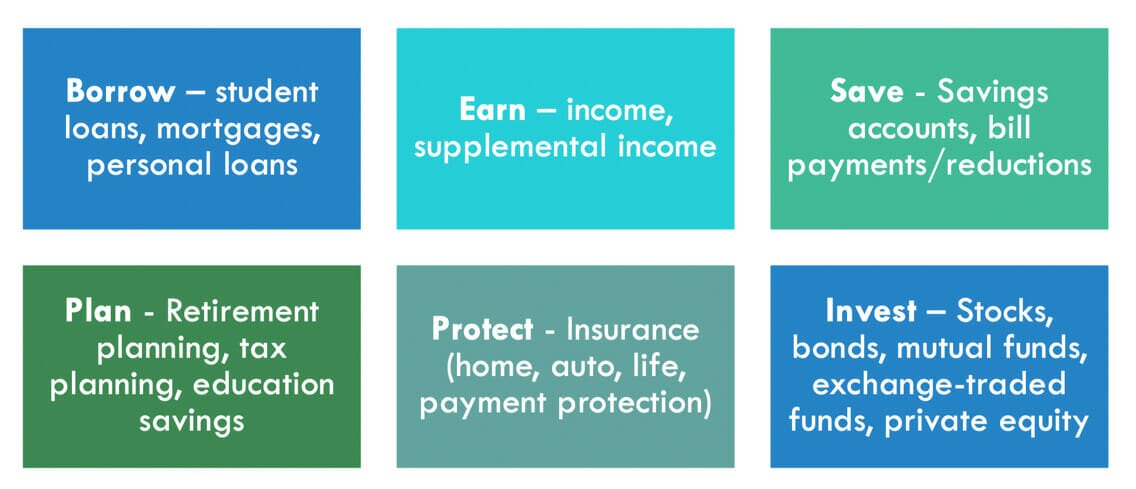

For most people, money is an instrument or a mechanism to trade in exchange for goods and services. Money is translated mentally into “incoming money” and “outgoing money,” or income and expenditure, respectively.

We can further break down this concept of money into a few categories.

Some of these categories involve spending money, such as “Borrow.” When people don’t have enough money on their own, they borrow. They do this either to make ends meet or to fulfill their aspirations, such as buying the desired item or using credit to grow their business. On the other end of the spectrum, investing puts your money to work. When you invest, your money makes more money on your behalf.

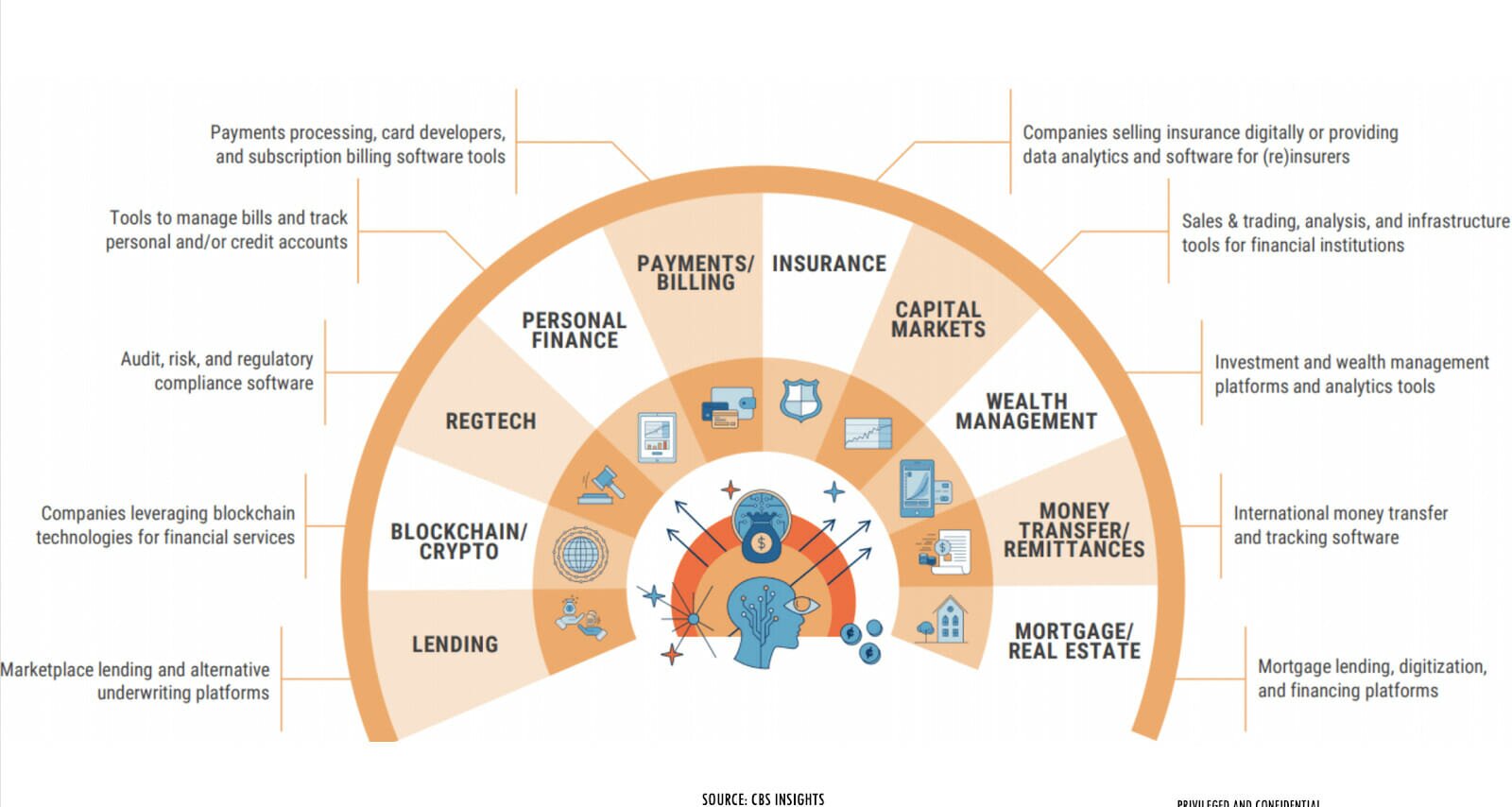

But the visual above does not present the full picture. Here’s a much better view of the fintech landscape that takes into account mental models of dealing with money, as well as infrastructure, regulations, methods of transacting, and more – all of which can influence your customers as they navigate the fintech landscape.

The Fintech Landscape

For more about fintech, I encourage you to listen to this conversation between Alex Rampell and Frank Chen. You can also learn more about mental models in the section below.

Customer Mindsets When Dealing with Finances

Regardless of the products you are building, you should be able to answer these questions:

- What am I solving?

- Why am I solving this?

- Who am I solving this for?

Once you know the answers to these questions, you’ll be better equipped to design a product that meets your customer’s unique needs.

One critical aspect of building financial products is the customer’s mental model or the “jobs to be done” with their money. While not every fintech product needs to address these aspects, this is a glimpse into the mindset of those either living paycheck to paycheck, and/or those striving towards a stable financial future. If you are further interested in this specific topic, especially as millions of people are dealing with the COVID-19 crisis and its financial impact, I highly encourage you to visit the Financial Health Network and the US Financial Diaries.

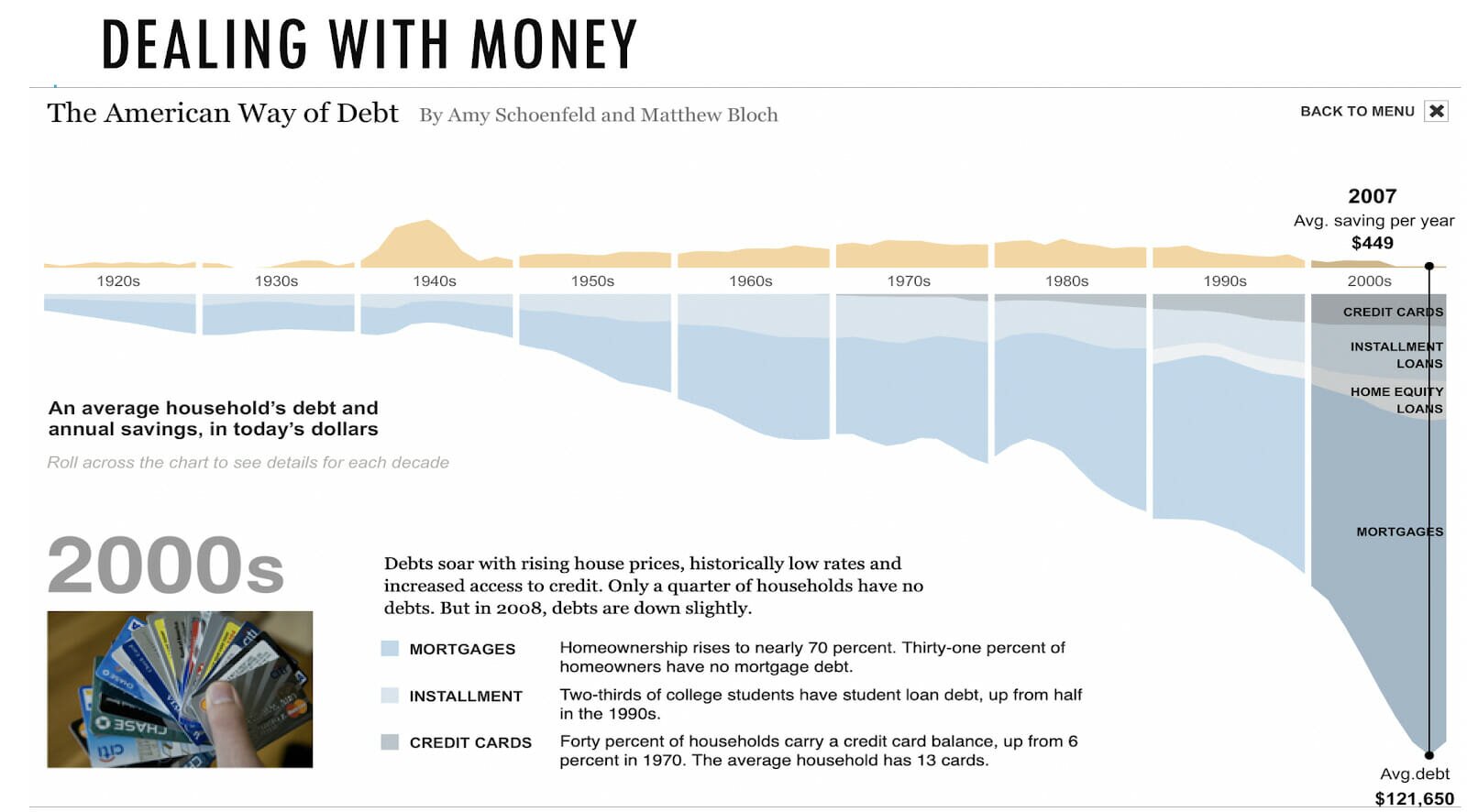

One major contributor to someone’s financial health and their attitude towards money is debt. Here’s a view of debt from the beginning of the 20th century to the early 21st century. If you follow the yellow versus blue graph, you will see that average savings haven’t changed much, but debt has skyrocketed.

Debt in the United States

Money is a cause for pleasure as well as pain — for those who struggle with debt, ‘money’ is not only a tool, it’s also a factor that induces stress, anxiety, and embarrassment.

Further, a customer’s “job to be done” could be something emotional like “I want to make investments on social causes that are interesting to me, but more so I want to appear cool to others.”

Note: this is not to argue that a meaningful product needs proper attention to all quants and/or quals. But hopefully, you see the nuance here in building financial products.

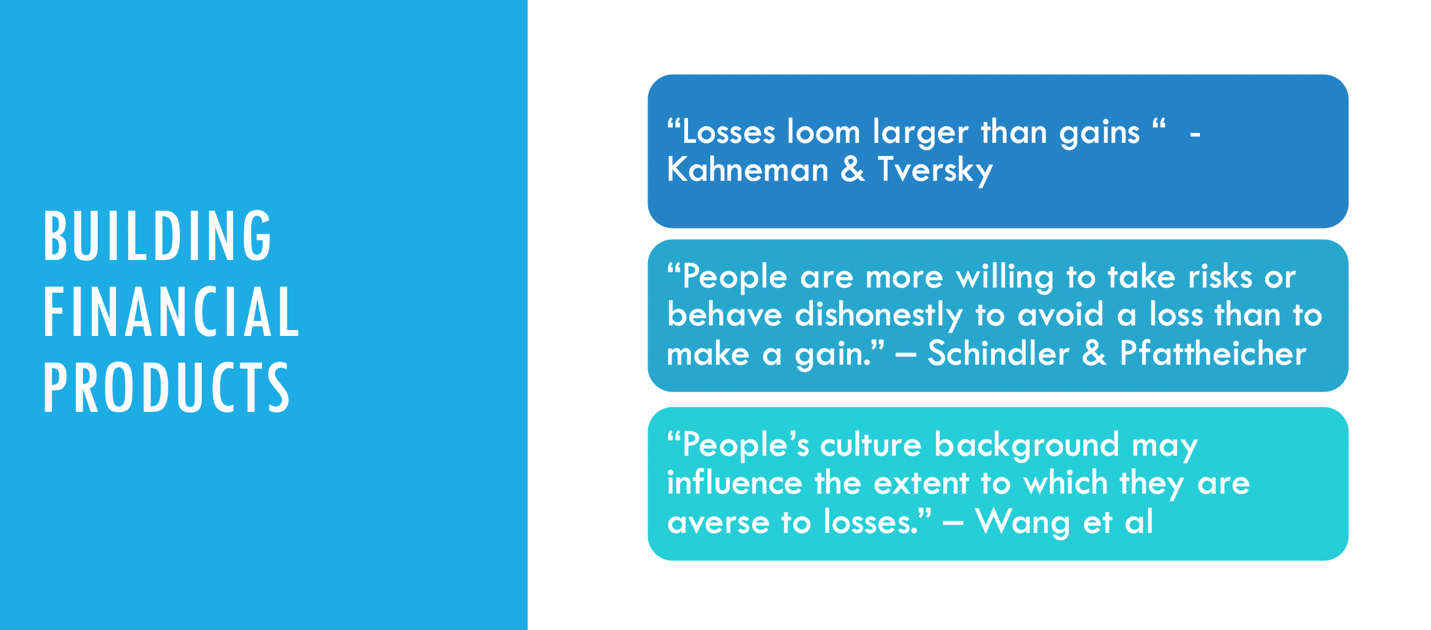

People also behave quite differently when dealing with money depending on their circumstances. Here’s a teaser on behavioral economics.

A better understanding of behavioural economics will reveal how your financial products work in the hands and minds of your customers.

I’ll wrap up this post with some quick tips on what to consider when building financial products. Please note this is not a comprehensive list and your regular management frameworks still apply here.

Quick Tips

Next, we’ll go into detail about the regulatory context and environment of the fintech industry, as well as how product managers might embrace this context to build products that add value and bring peace of mind to customers.

The Regulatory Environment in the Fintech/Services Industry

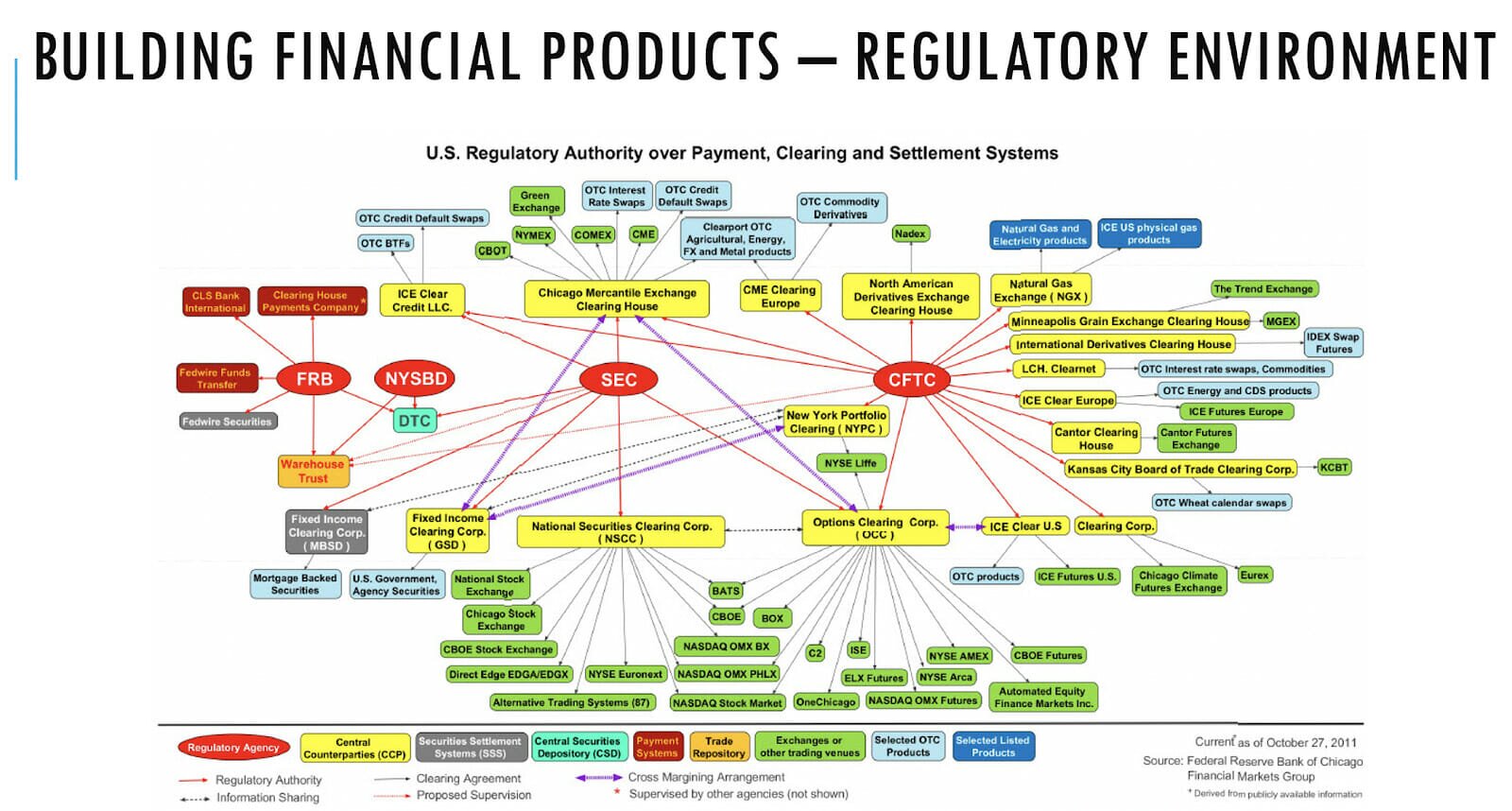

A picture is worth a thousand words…like this snapshot of the fintech regulatory environment.

Fintech Regulation at a Glance

While this is not comprehensive, depending on the type of product and/or vertical within the financial industry, your products and processes are subject to one or more fintech regulatory frameworks. These are developed and enforced by several agencies and organizations.

Why These Regulations Matter

The fintech industry differs from other tech industries because your products may intentionally or unintentionally harm people if they are left unregulated. Furthermore, you, your team, and/or your company is subject to several industry laws and regulations. These laws and policies, which have often taken several decades to develop, ensure your products don’t harm people in any way.

Although building financial products comes with a “price”, it is one of the most satisfying in terms of value and impact to product managers and their customers. Your products could be used every day! Think of the customers who rely on your product for guidance through their financial chaos and worries. Your products could even help someone plan their future, such as deciding how much to save for retirement, or which school they should send their kids to and how they might plan for it.

I would also say that financial products could touch the minds and hearts of people in a very meaningful way compared to other products. What you build today could alleviate certain people from poverty and hunger and offer a cushion against unforeseen emergencies.

Is Building Financial Products a Slow Process?

Well, it’s good you are asking that question! As a product manager, your instinct may be to move super-fast. But given the stakes of your products, you ought to proceed mindfully and cautiously.

That doesn’t mean you can’t move quickly, though! I’ll show you some ways of doing so, all taken from my own experiences. You’ll learn how to build products at a pace that balances your needs with industry regulations.

As a fintech product manager, you are not only bound by regulations but also by the number of cross-functional teams you need to deal with. I’ll talk more about them in another post, but here are some examples of stakeholders you might need to work with.

How to Approach Things Differently Given Regulatory Context

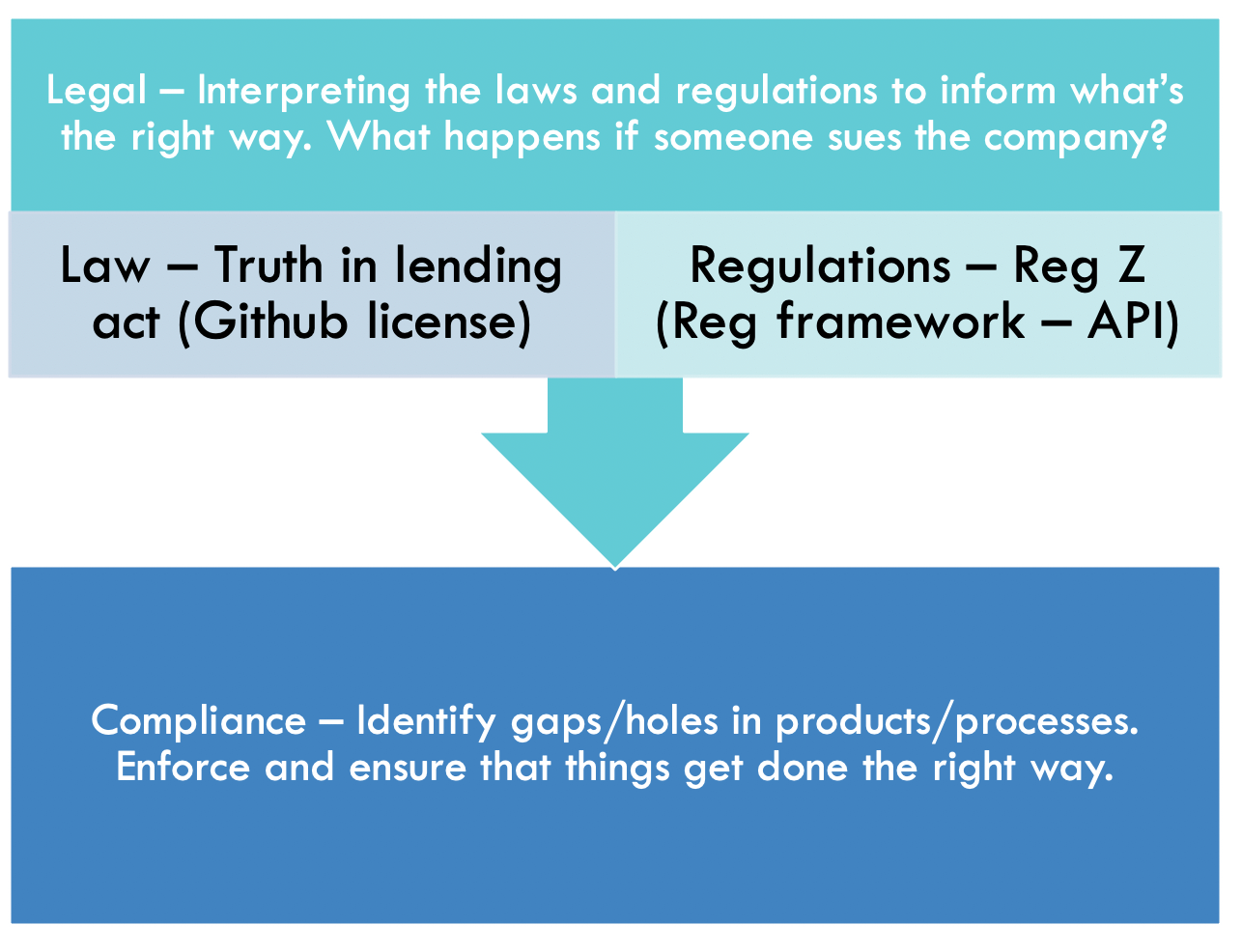

First, you need to understand the difference between legal and compliance – what roles and responsibilities each one has, and how you should partner with them. One way to think about the differences, especially for technical product managers, is this analogy using Github and APIs.

Legal vs. Compliance

If you are new to fintech, learn your team’s best practices in addition to going through your company’s legal and compliance training. Also, realize in small and simple examples of what each law means and the corresponding product interpretation.

Legal and Compliance Best Practices

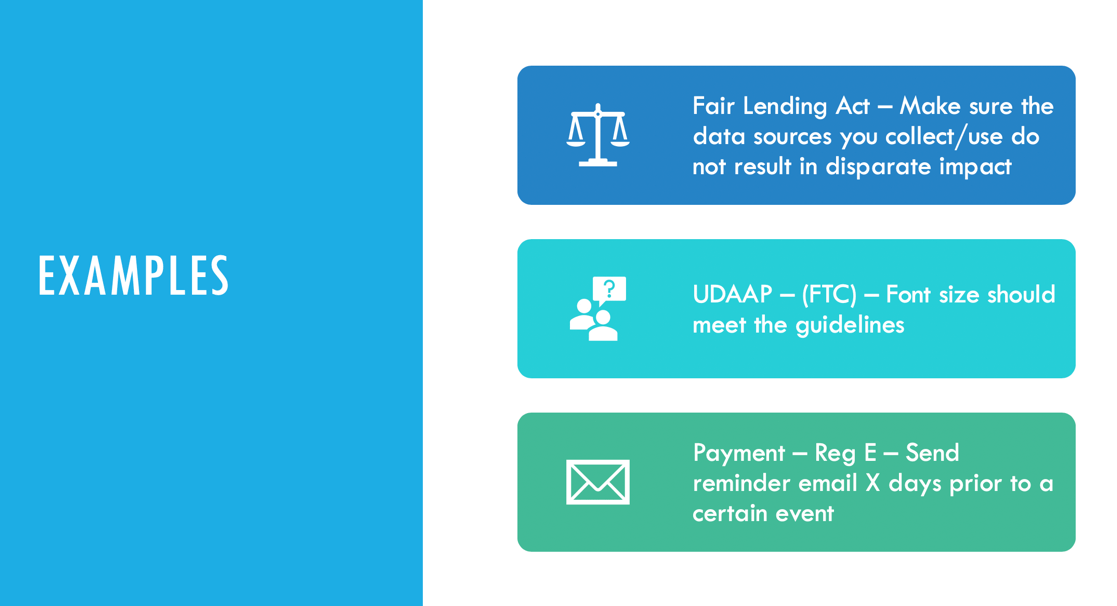

In each of the above cases, there’s a specific role for you as a product manager.

- If you are exploring alternate data sources or using existing data in new ways, work with your data teams to evaluate that there’s no disparate impact in your solutions.

- Work with your design team to ensure that font size for user-facing messaging meets the regulatory guidelines.

- Work with your marketing team to ensure timely delivery of emails as per the regulatory guidelines.

The legal/compliance folks, not the product managers, are responsible for interpreting laws. Your job is to understand the guardrails and figure out how you ideate within that scope. Great PMs go a step further to realize how we might work with the right stakeholders internally and externally to evangelize new policies that serve the best interest of customers and the rest of the stakeholders.

Work with your regulatory affairs counterparts to take your work to new heights! See below for some quick thoughts on this topic.

How to Move Fast Despite the Regulatory Environment

Fundamentally, the way to speed up your product launch cycles is to identify the points of friction, and then work to remove them. In a regulated environment like fintech, your biggest points of friction are likely to be around legal and compliance oversight, and interactions / hand-offs with your regulatory teams. Lucky for us, building trust and improving velocity with cross-functional teams is something that product managers aim to be good at, so we can build on our existing skills!

With that in mind, here are a few ways to improve the velocity of your product launch cycles:

Increase Confidence and Trust Between Legal / Compliance and Product Teams

- Becoming aware of regulatory guidelines and the legal and compliance processes in the company. Being on top of your organization's required Legal and Compliance training is the first step.

- Laws and Policies are not a binary rule — understand the nuances on the do's and don'ts

- Understand how competitors and non-competitors approach their Product strategy to deal with regulatory affairs.

- Socialize not just with Product Managers, Engineerings, and Designers but make your Legal/Compliance counterparts your allies.

Operationalize Your Legal / Compliance Needs

- Engage Legal and Compliance early on in the product discovery phase. Establish a regular cadence for your product reviews with legal/compliance teams.

- Look for alternate solutions including vendors and partners who can help solve your regulatory challenges.

- Reduce round trips: Get alternate designs/COPY approved ahead of time. Especially if you are experimenting and need multiple variants, get them reviewed and approved in advance, so you are not expending your learning cycles.

- Make the guardrails visible and clear to product teams, so they know their boundaries on how far to push the product.

Alternate Approaches

There are probably very few domains such as fintech and health-tech, where once a brand affinity is established customers will give away their information in a heartbeat. To build brand affinity, you may have to start slow by establishing the right frameworks, developing a good understanding of regulations, communicating, and collaborating with regulators, etc. Product Managers can help accelerate the process of getting things in order by exploring new ways of testing approaches under regulatory watch – examples of doing small scale product testing could be achieved using regulatory sandboxes.

The legal and compliance team’s role is to guide the business and product functions by providing the assessment of risk after evaluating the product strategy, proposals, and solutions. They may have a strong point of view on recommending fixes, however, it’s often the responsibility of the business owner to make those calls on what level of risks to bear. Product Managers are the best positioned to provide an input function to business owners to make the right call. Some of the considerations include reducing the number of customers who see the new experiment or product, setting a budget to handle any forthcoming regulatory risks.

Product Managers are the best positioned to provide an input function to business owners to make the right call.

While doing experiments at any cost is never a good strategy, teams can decide their course of action by evaluating if the tradeoff on risks is well worth the benefit of expedited learnings, anticipated customer complaints, etc.

I hope you enjoyed this guide to excelling as a product manager in fintech, and I hope you’ve gained a deeper understanding of the customer mindset and their jobs to be done. You should also have received context on the regulatory framework and learned how to build products that add incredible value and bring peace of mind to customers.

I’ll leave you with some thoughts on how you might build better fintech products.